01 May

2023

What is the future of fintech?

After a phase of euphoria, the fintech sector has entered a period of maturity, refocusing on the fundamentals of customer value, growth, and profitability. Nevertheless, the role of fintechs as a catalyst for change in financial services is undeniable, reinforcing the need for established players in banking and insurance to capitalize on this new competition. This notably requires accelerating the adoption of new technologies and establishing successful partnerships with fintechs.

Euphoria has subsided in the fintech space

The fintech sector is experiencing the episode of turbulence after years of double-digit growth. The valuation of fintechs fell sharply between January and July 2022. The success story Klarna, for example, suffered a drop in valuation of around 85% in July 2022 compared to its value in June 2021.

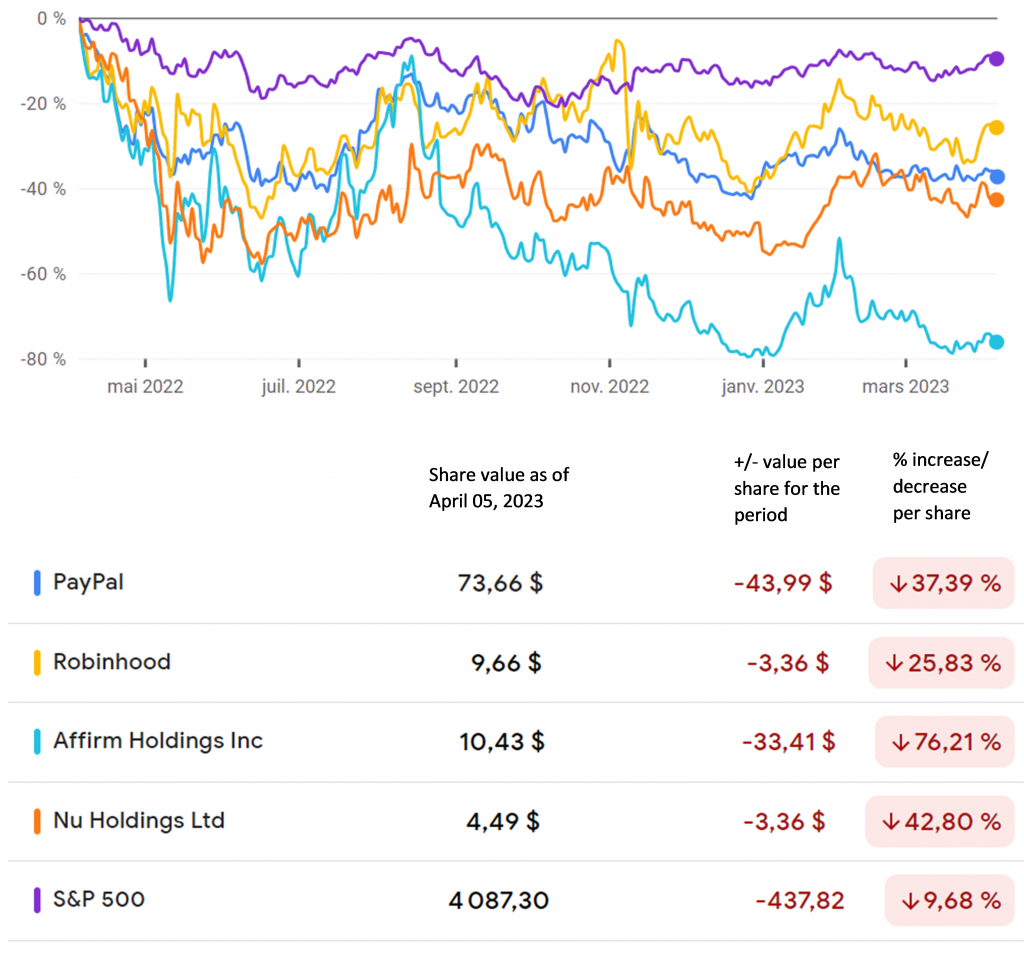

Evolution of stock market valuations on the NYSE over the last twelve months

(Source: Google Finance)

This crisis has also led to massive redundancy plans (Klarna, Robinhood, Paypal, Better.com).

Finally, the cryptocurrency sector has experienced an unprecedented crisis with high-profile bankruptcies (Terra Luna, Crypto Celsius, … including a financial scandal with $8 billion in hidden losses for FTX). All these elements, widely reported by the international press, have contributed to tarnishing the image of fintech, which, as late as 2021, was often presented as the future of banking and finance.

The upward spiral that allowed some fintechs to overtake large traditional banks in valuation during the Covid-19 crisis thus seems to have been completely reversed.

However, this must be qualified.

While the crypto bubble has burst, for other fintech models, this is instead a healthy correction.

The sector is now recovering from the fundraising and valuation spree witnessed in the second half of 2021. The macroeconomic context has caused a contraction in the previously abundant financial liquidity, while investors are now less willing to take risks in a much more uncertain economic environment. The combination of these two factors means that fintechs now need to refocus on the fundamentals and therefore be profitable, to attract investors.

The impact of the macro-economic crisis varies according to the fintech business model

To get a better idea of the impact of the macro-economic crisis, it is worth looking in more detail at the different fintech segments as these impacts are very different from one business model to another.

The most mature segments of the market (B2B payment solutions, cybersecurity, infrastructure) have been less impacted by the valuation drops and downsizing as they continued to benefit from the enthusiasm and financial support of funds. On the other hand, players operating in the field of credit or neo-banks are being hit hard by the paradigm shift. More generally, models that have failed to demonstrate their ability to achieve positive profitability are more affected by the crisis.

In addition, some channels are under regulatory scrutiny, which could hamper their ability to develop, as they could soon be further constrained by more stringent regulations. For example, BNPL (Buy Now Pay Later) products are now being singled out by the financial authorities, who are concerned about the risk of an explosion in over-indebtedness and the shortcomings of certain neo-banks in terms of risk management and the fight against financial crime. Since the sanctions imposed by the BaFin and the Bank of Italy, N26, for example, has been forced to curb its growth.

In a market that is already saturated with banking offerings, streamlining expenses will not allow neo-banks to survive in the long term. Indeed, the competitive advantage of neo-banks lies mainly in the customer experience (state of the art digital application and simplified customer journey) and the ability to offer competitive rates. However, over time, the customer experience advantage tends to fade, and their incomplete product line does not allow them to generate sufficient revenue to achieve profitability. In short, to survive, neo-banks will have to become “real” banks, i.e., expand their range with more profitable banking products, but subject to regulations that they have so far managed to avoid.

The context is radically different in countries where a large part of the population is still poorly banked, typically in certain emerging countries. In these countries, neo-banks can more easily reach their break-even point with a fairly basic product and service offering at the outset, which they can then expand, through partnerships, if necessary, to increase revenue per customer. These models, like Nubankwhich, are already profitable and have been relatively unaffected by the crisis.

Beyond the crisis, fintechs are catalyzing change in the financial services industry

The media hype surrounding the high valuations of fintechs has for a long time tended to reduce them to the role of cash-machines for performance-seeking investment funds. However, the emergence of these new players is helping to transform the financial services market much more profoundly than it appears. In essence, fintechs use technology to deliver innovative value. Through their innovation and agility, fintechs are exploiting failures in the existing system, capturing market share, and driving some structural changes in the industry. For example, neo-banks have completely changed the way banking is used and the standards of everyday life: simplified customer paths, a 100% digital relationship and bank branches that are no longer used. Stripe has revolutionized the small business payment services market by choosing, unlike traditional banks, to trust businesses a priori and assess their risk profile by analyzing the actual transactions made on their account.

These structural changes in the financial services sector have led to major transformations in the banking sector. Traditional banks have followed the example of neo-banks by developing their own integrated digital applications, with considerable resources. To achieve its 2017-2020 roadmap, Société Générale has spent nearly two billion euros per year on transforming its information systems. Similarly, all banking networks now offer BNPL options to their customers, that were still unknown in most European countries a few years ago.

The winning fintech models are those that provide a relevant response to customer needs that are poorly met by traditional banks, or that exploit efficiency technological levers. Far from being a passing phenomenon, these new players are changing the rules of the game and helping to reshape the financial services galaxy. Fintechs still seem to have a bright future ahead in a market that is still dominated by traditional players disadvantaged by less than agile models.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}