03 Feb

2021

Retail banking must undertake its revolution

France is the Europe’s leading country …

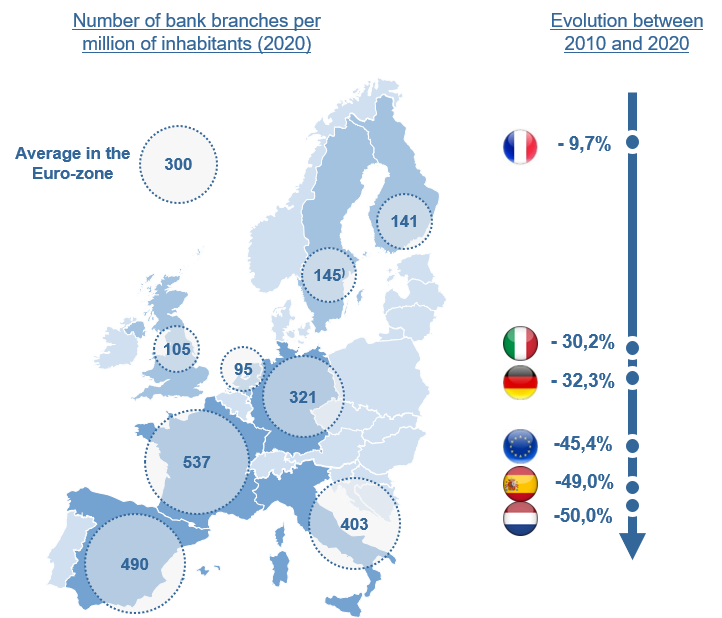

With nearly de 36,000 bank branches, i.e., one for 1,860 inhabitants, France is now at the top of the European ranking, ahead of Spain which until recently occupied the top spot.

With nearly de 36,000 bank branches, i.e., one for 1,860 inhabitants, France is now at the top of the European ranking, ahead of Spain which until recently occupied the top spot.

Unfortunately, that’s nothing to be proud!

Since the early 2000s, bank branch attendance has been steadily declining, despite the efforts made by banks to deploy innovative branch concepts. The old-fashioned look of counters and POS displays was refreshed by interior designers who conceived new reception areas including contemporary-style furniture, ambient lighting and fragrances, texture and color combinations. This is a commendable effort, but it is not enough to halt the decline in bank branch visits that has been observed throughout Europe. Most of our neighbors have understood this and have chosen to adapt by reducing the number of bank branches per capita by 30 to 50% over the last decade. France is the exception, with a decrease of barely 10% over the same period.

The growing disaffection with branches is a natural consequence of digital banking services. Electronic payments have largely replaced cash and scriptural payments, the information customers need is accessible 24 hours a day from their PCs or smartphones, and most problems can be solved remotely by simply calling the Customer Relationship Center or by e-mailing their advisor.

The shift to digital is inevitable: it does not only meet consumers’ rising demand for convenience and responsiveness. It also helps to improve the operational performance of banks, with customers processing their transactions independently (self-service banking).

Digital banks are gaining ground

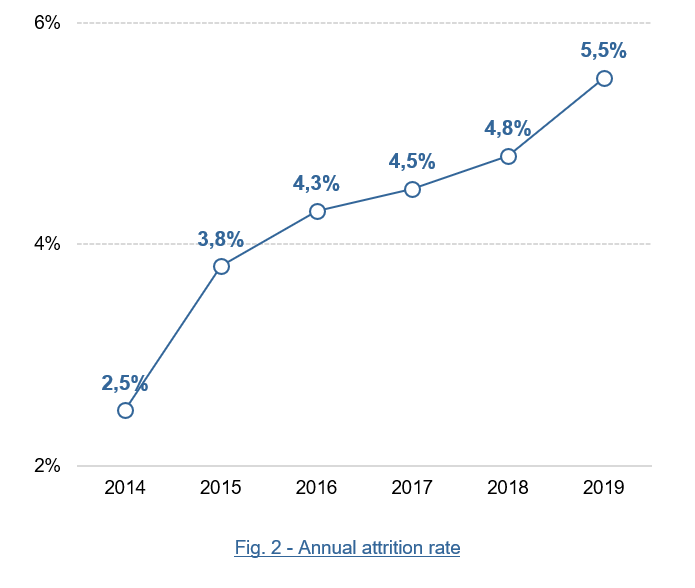

Customers are not only eschewing bank branches, but they are also becoming less loyal. The customer attrition rate has more than doubled in a few years (see figure 2), and this is particularly true for the most profitable customers. Indeed, attrition reaches nearly 10% per year for customers with more than €80,000 annual income while it does not exceed 3.6% for those with less than €20,000 annual income.

This evolution benefits mainly online banks and neo banks which are considered more innovative and agile, and less expensive than traditional banks. Over the last decade, digital banks have won more than one in ten French customer and the pace is accelerating: they now account for nearly a third of all new customers.

A growing trend intensified by the health crisis

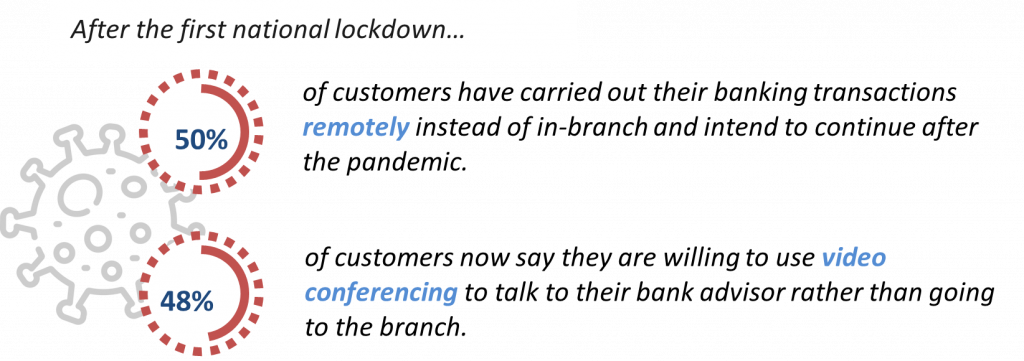

Customers turning away from their bank branches is not a new phenomenon in France. The average number of bank branch visits is estimated to have been halved over the last decade. Only one customer in five is still regularly using branches (i.e., once a month). This trend has become even more pronounced during 2020 due to the health crisis. A survey by ValueQuest conducted after France’s first national lockdown found that half of the customers now prefer web-based interaction or video conferencing, rather than traditional interaction with bankers in branches.

The habits acquired during the health crisis will therefore permanently change behaviors toward banking, with customers deserting branches.

In addition, bank employees, including advisors, were usually forced to telework (at least partially) during the crisis. Under pressure from public authorities, workers representatives and employees themselves, there is no way back and most banks have already planned to make teleworking permanent for about two days a week. In summary, bank branches were first abandoned by customers, they are now also abandoned by the employees themselves.

Should it be held that game is over for traditional banks and that the next step is simply to capitulate and close their « beloved branches », to be able to compete on equal terms with neobanks?

Assuming that this scenario is « socially acceptable », it might be the wrong strategy for major banking networks. Indeed, although branches can be considered a burden, they might in fact be the main competitive asset for networks to maintain their dominant position.

The bank advisor as a lever to improve the online customer experience

Even if customers clearly show appetite for the simplicity and immediacy of digital technology, they are still very attached to their bank advisor and to receive guidance on structural choices concerning their savings or their projects and related financing options. Yet, the most demanding are not those expected: 40% of young people under 30 say they prefer to speak to an advisor in a face-to-face meeting in a branch (compared to less than 20% for those aged 30-45).

There is no doubt that tomorrow’s banking is digital, but the prime driver of success might be what some describe as a new form of augmented reality, where the human world improves the digital world to get « augmented digital ». Using the best of technology as a source of contact, while giving access to personalized and expert assistance through an advisor offering customers the relationship quality that machines will not be replacing anytime soon.

In this respect, network banks are outperforming their digital competitors, with the number and quality of advisors in branches. Now it is up to them to take advantage of this situation…

Retail banking: the time has come for revolution

There is no doubt that the number of bank branches will have to be reduced, especially in urban centers where they are highly concentrated. Fewer but larger branches, designed to brilliantly represent the bank standard, where customers are offered immersive experiences and a range of support regarding their financial and insurance issues.

There is no doubt that the number of bank branches will have to be reduced, especially in urban centers where they are highly concentrated. Fewer but larger branches, designed to brilliantly represent the bank standard, where customers are offered immersive experiences and a range of support regarding their financial and insurance issues.

As per the flagship store concept developed by the major tech brands, the next-generation branches will be equipped with interactive terminals offering information and guidance to customers. They will be using biometric identification and provide their customers with a fully personalized, electronically subscribed paperless offer. Unless they prefer human contact with advisors equipped with tablets in comfortable purpose-designed work pods introduced within the branch workspace set up.

It will therefore be necessary to rethink the branch concept in terms of layout and physical organization. But above all it will be necessary to change sales practices and culture. Sovereign customers are more than ever the center of attention. They are free to use any way to interact with their bank whenever they like. The somewhat rigid concepts of customer portfolio and sales plan based on product marketing strategies will have to change into omnichannel marketing and customer-centric sales strategies driven by artificial intelligence analysis of data and customer insights.

Retail banks only have a future if they are up to meet huge challenges and are ready for revolution.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}