02 Sep

2025

Asset Managers Facing Profitability Challenges

The asset management industry has long benefited from a highly favorable growth model: a historically low fixed-cost industry with growing demand driven by both global savings growth and the mechanical rise of financial markets. Additionally, various financial and health crises have led to massive liquidity injections, causing a significant increase in asset prices, until central banks adjusted their policies.

Furthermore, due to the importance of investor protection, the industry has benefited from regulations that raised barriers to entry and maintained fee structures that, until recently, remained largely unchallenged. Asset management was one of the most profitable financial activities, boasting high gross margins and an exceptionally high Return on Equity (ROE) compared to other financial sectors, all while operating under relatively low capital constraints.

However, despite its profitability, the sector has faced growing challenges and ominous signs for more than a decade. So, how much longer can we refer to it as the “golden goose” of the financial industry?

A Strategically Important Industry

Economies today face two major challenges: technological advancements and the green transition. While both revolutions are expected to yield benefits in the medium to long term, they share one key characteristic – a massive need for financing. In Europe, where businesses are structurally undercapitalized compared to their U.S. counterparts, neither governments nor banks can meet these financial demands alone. Governments are constrained by high public debt, while banks are limited by the size of their balance sheets. However, Europe enjoys an exceptional level of household savings.

Asset managers are thus expected to play a crucial role in directing these savings toward financing strategic projects, acting as intermediaries between household portfolios and corporate capital needs.

Consequently, the asset management industry is central to governments, which rely on it to channel investments in line with their political priorities—such as industrial reshoring, combating climate change, supporting SMEs, and developing strategic economic sectors. Moreover, governments depend on institutional investors to finance long-term debt. With public debt levels reaching historic highs, the investment capacity of asset managers has never been more politically significant.

Increasing Pressure on the Industry

Despite its strategic role, the asset management sector faces a challenging environment marked by economic uncertainty, regulatory changes, competitive pressure within the asset management value chain, and technological disruptions.

The industry operates in a rather unstable macroeconomic environment. Since the COVID-19 pandemic, global economic growth has slowed, while inflation remains a persistent threat. Rising public debt levels contribute to financial market instability, and geopolitical tensions heighten risks and exacerbate economic uncertainty. Furthermore, the growing economic divide between Europe and the U.S., along with the rise of protectionist policies worldwide, complicates economic forecasting and makes investment decisions even more delicate.

Regulation is another major transformation driver. Directives such as SFDR, MiFID, IDD, and the RIS (to name a few) have significantly increased regulatory costs. At the same time, national and EU authorities are exerting mounting pressure to lower retail investment costs. Product offerings are increasingly constrained, particularly due to the near-mandatory integration of ESG-compliant investment vehicles. Consumer protection, the creation of a single European financial market, and the proactive policy of directing savings toward ESG investments all come with costs that European asset managers largely bear.

Within the value chain that delivers investment products to end consumers, not all players contribute equally to cost reductions. Asset management firms find themselves caught between index and data providers with near-total pricing power and distributors—strengthened by digital platforms—who push to lower final prices while maintaining their margins.

Finally, technological advancements are reshaping the industry. Automation, robo-advisors, and artificial intelligence are optimizing processes but require significant investment. Personalization and digitalization of the client experience have become essential expectations. Additionally, emerging asset classes such as crypto assets are altering traditional investment strategies, necessitating new resources often beyond the expertise of traditional asset managers.

Economic Performance Under Pressure

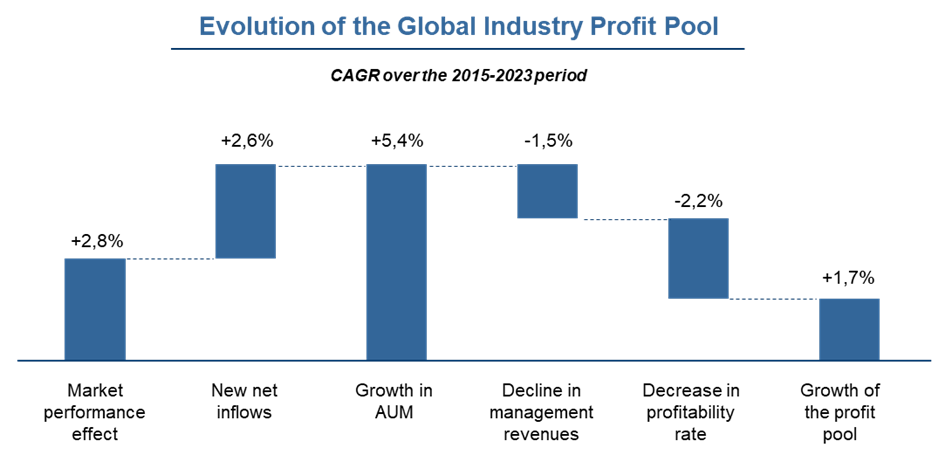

Industry-wide forces are putting asset managers’ business models under increasing strain, affecting growth in assets under management, average margins, and overall costs. While the global asset management industry still demonstrates profit pool growth (see graph below), individual players may experience far less favorable trends.

Asset growth continues to benefit from net inflows worldwide and market effects. However, new asset classes are increasingly capturing inflows. Index-based investing, for instance, has gained substantial traction—especially in the U.S., where 90% of net inflows over the past decade have gone to passive funds. Similarly, “star funds” with strong historical performance are must-haves for distributors, while low-risk assets like euro-denominated life insurance funds and regulated savings products remain popular choices. Traditional active asset managers who cannot compete in the index fund market are fighting for a shrinking share of inflows, leading to potential outflows from asset classes deemed expensive and risky.

At the same time, the average margins collected by asset managers are under intense pressure from both distributors and regulators. Distribution remains a critical link in the value chain, as client access is still dominated by banking and insurance networks. The rise of distribution platforms has further empowered distributors, increasing their ability to negotiate with asset managers. As a result, asset managers must justify their margins more than ever—particularly given regulatory demands for greater transparency (MiFID) and requirements to prove that fees provide value (“Value for Money”).

Cost pressures further complicate the industry’s economic equation, with global asset management expenses growing by an average of 4% to 5% annually. This cost inflation stems from rising regulatory demands as well as the necessity to invest in technological advancements. Every function in the asset management chain is being transformed by automation, enhanced data utilization, and AI-driven process management and decision-making. However, mastering these technologies requires new skill sets – such as data scientists and digital experts – who are often absent from the industry’s traditional talent pool. As a result, firms struggle to achieve the expected cost savings from digitalization.

Conclusion: The Need for Action

Given these challenges, asset managers must act on multiple fronts. High-profile mergers announced last year are only the top of the iceberg. While the creation of “European champions” may strengthen some firms, it does not fully address the industry’s underlying challenges.

Like all financial services, long-term value creation requires firms to identify their key areas of excellence. Whether by building strong client loyalty, attracting new customers through superior service, or offering differentiated products with compelling investment profiles or pricing, non-distinctive players are at risk.

Ironically, while passive investment strategies are thriving, the future of the industry will belong to those who take a highly “active” approach to their industrial strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}