15 May

2020

Responsible investment: fad or groundswell?

Corporate social responsibility and commitment to the general interest are now an essential part of the communication of major groups. The financial industry, whose reputation has been damaged over the past decade, is no exception to this trend and is counting on these issues to restore customer confidence. For financial institutions, Responsible Investment (RI) is one of the levers for moving from words to action.

Beyond the hype, asset managers are increasingly considering environmental, social and governance (ESG) criteria in investment. Responsible investment has been growing exponentially in France over the past twenty years, reaching more than €1,458 billion at the end of 2018 (source AFG, July 2019). With an increase in assets under management of around 40% between 2017 and 2018 and a broadened spectrum of asset classes, the RI market poses many challenges for asset management companies: reputation, risk control, differentiation, growth, etc.

A market in the process of standardization

However, the lack of a clear and uniform definition, as well as the heterogeneity of practices are major obstacles to RI understanding and development. However, progressive standardization is underway: international standards, a common language (European taxonomy), regulations, labels (SRI, Greenfin), extra-financial rating agencies, and other ethical stock market indices are gradually giving structure and credibility to the responsible investment field.

Furthermore, ESG criteria are now fully part of the business of asset management companies through the scaling up of “ESG integration”, which consists in incorporating some of these extra-financial criteria into the analysis parameters used to build portfolios. Again, although they remain largely unstandardized, there is every reason to believe a gradual standardization will be observed like in credit ratings, for which harmonization has significantly increased over the past 40 years.

Responsible investment and profitability: towards a consensus

At the current state of evidence, it is not that easy to precisely assess the added value of integrating such criteria into investment policies.

Skeptics consider that restriction of the investment universe could reduce potentially profitable investment opportunities, while ESG-compliant companies may incur expenses that could affect their financial performance; not to mention investors might also be penalized by ESG-induced additional costs.

Optimists argue that a deeper fundamental analysis helps to capture factors that could potentially harm a company’s performance and reduces the investment’s risk. RI would direct investment towards companies with sound governance, which would tend to protect the performance and reputation of investors over the long term. In addition, the climate challenge, the expected tightening of environmental standards, and the incentives for reducing carbon footprint (notably tax incentives), could logically bode well for the most virtuous companies.

However, a consensus emerges that RI funds would perform at least as well as conventional funds. The performance of RI, like “traditional” investment, would therefore be more dependent on the quality of the research, a careful selection of the assets in portfolio, and relevant investment strategies.

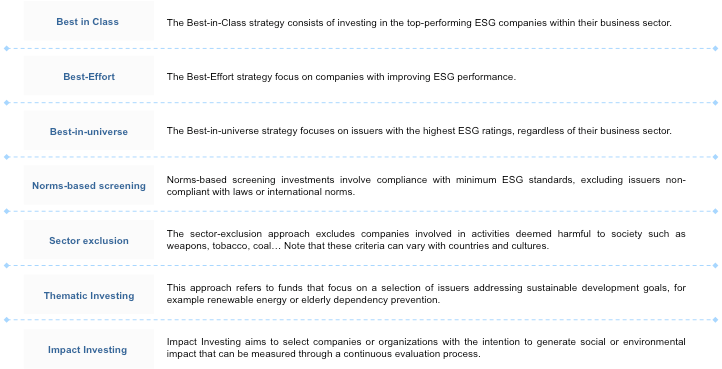

A wide range of approaches, offering great freedom of action

The growing importance of extra-financial analysis in the investment process has led to the adoption and development of a wide range of RI strategies. Here are some significant examples:

These various RI approaches can be combined with each other, which allows great flexibility, offers a wide action scope, and enables different levels of “commitment”. In the context of ever-intensifying competition and seeking new modes of differentiation, RI is a chance for asset managers to stand out.

A market driven by legislation and offering solid growth prospects

If RI has many dimensions, the environmental theme is one of the main drivers of the sector (as evidenced by the expansion of the Green Bonds market in recent years). Widespread awareness of the risks associated with climate change and their economic impacts have thus led to the development of French regulations that enhance market growth.

As expected, RI is most successful with institutional investors, who are required to transparently share how they integrate ESG parameters into investments, as per Article 173 of the French Ecological and Energy Transition (TEE) law of 2015. Thus, in order to remain eligible to tenders, asset managers can only adapt to these requirements. As the TEE law (which will tend to become increasingly stricter) is an important step in the commitment of financial players, other regulations will emerge, particularly at European level. Anticipating these evolutions will be a key differentiating factor.

With regard to the consumer segment, there is still considerable room for growth, although employee savings schemes, also encouraged by legislation (PACTE law), contribute to the segment’s momentum. Responsible investment is still little known to individual investors, and for good reason: it is currently poorly understood by advisers and rarely offered in the distribution networks. However, asset managers are getting ready to attract this clientele and are revising their strategies, notably by promoting more “aspirational” approaches. For example, the Best-in-Class approach, which mostly defines the French RI market, can inhibit individual investors’ enthusiasm and understanding, while the development of impact and thematic investing could provide a more appropriate response to the expectations of individuals seeking soundness and clarity.

A strengthened legal framework and more standardization will provide guarantees of transparency and quality about extra-financial criteria and investment policies. At the same time, additional communication and educational efforts will reassure and give more visibility to savers for whom profitability is key. These are all opportunities to strengthen dialogue and mutual trust between asset managers and investors.

Rome was not built in a day

Despite this positive outlook, the development of RI is a challenge for asset managers and requires significant investments. In order to deploy reliable offerings, it will be necessary to strengthen data research and management, refine methodologies, standardize models while keeping agility, but also to monitor performance, implement dedicated governance, develop in-house skills and forge links with new partners (data and analysis providers). Moreover, if environmental concerns have been brought to the forefront, social and governance aspects are not at this stage fully understood by stakeholders. This is long-term work for organizations that will have to look beyond regulations and develop long-term strategies.

This is a challenging step to take but market growth will also strengthen gradually, through combined initiatives from both private sector players and the regulator’s. These initiatives will be part of a profound societal transformation and RI might over time become the new standard. The asset managers who will prove able to anticipate the trends and have proper and accurate understanding of this temporality will stand out.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}